With unexpectedly strong economic data and investors’ AI enthusiasm driving the S&P 500 32% higher over the past 12 months, some experts are worried that the stock market is in a bubble. Bank of America head of U.S. equity and quantitative strategy Savita Subramanian definitely isn’t one of them, but after raising her year-end price target for the S&P 500 from 5,000 to 5,400 last week, she took the relatively unusual step of saying she’d heard from quite a few market bears.

Subramanian said in a Monday note that she had a “full week of feedback and pushback” since making her bullish call, including a direct question on a call that went something like: “Savita, are you forecasting a bubble?” The answer to that question is no, Subramanian insists—and she’s ready to address the concern.

In an FAQ issued by Bank of America Research, the veteran analyst explained that despite all the fears over a potentially irrationally exuberant market, prior market bubbles have typically featured a few key factors—mainly “a gap between price and intrinsic value” and “rampant speculation”—and the current market doesn’t fit the bill. “Housing in 2007, tech in 2000, tulips in 1637 are examples that tick these boxes. But the S&P 500 today does not,” she wrote.

Still, with AI fervor harkening back to the internet era as it pushes some tech stocks ever higher, a few Wall Street experts have made comparisons to the dotcom bubble. Now, there’s an argument over whether we’re repeating 1995, and the tech bull run is just getting started, or whether it’s more like 1999, and a crash is right around the corner.

Subramanian reassured readers that, in her view, it’s “more 1995.” From investors’ relatively subdued sentiment levels to rising productivity and the fundamental strength of Big Tech leadership, this isn’t a bubble just yet.

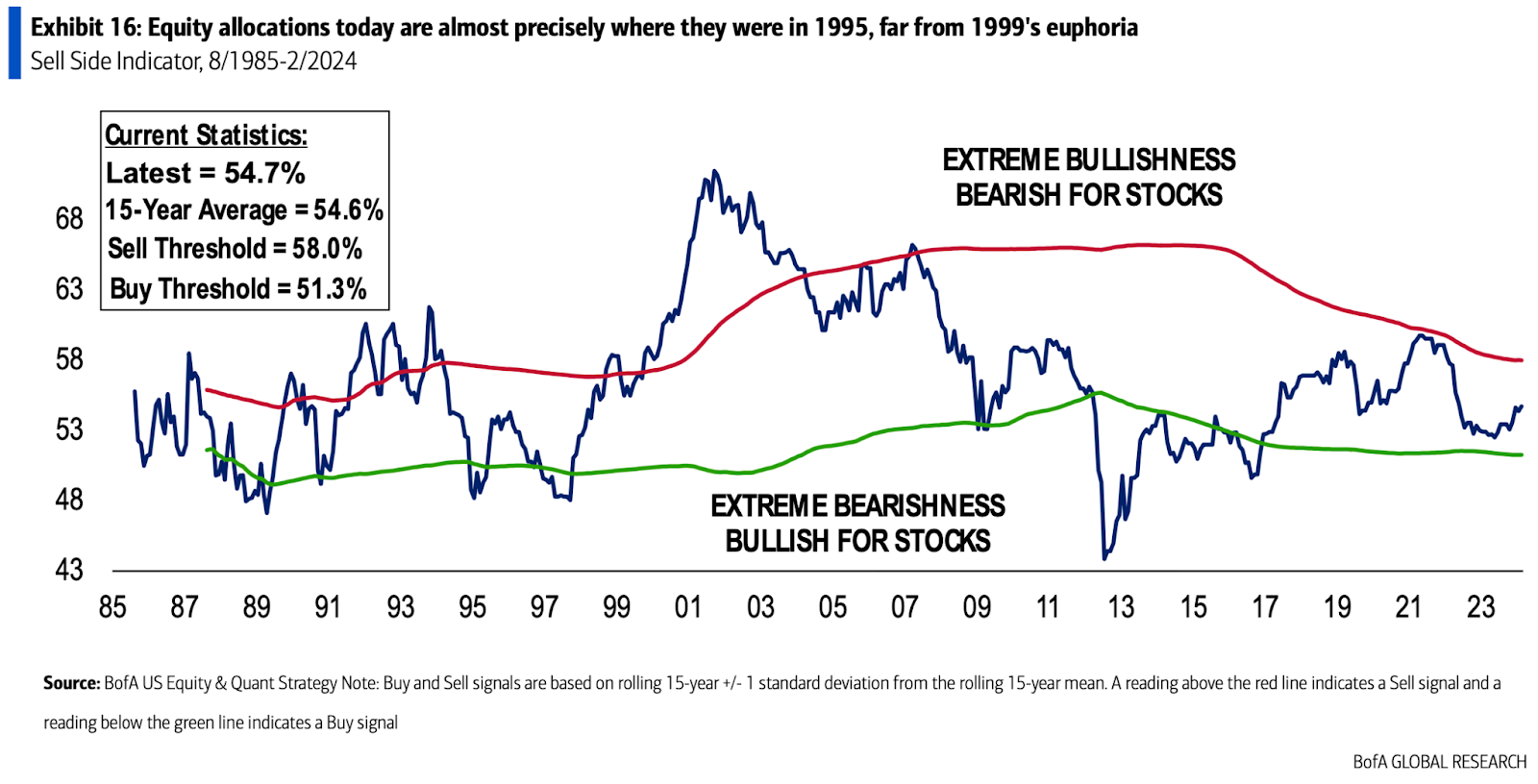

Stocks are overvalued, right?

The first criticism of Subramanian’s bullish prediction for the S&P 500 has to do with market valuations. The S&P 500 currently trades at roughly 20.5 times forward earnings, compared with an average of 15.8 since 1986, according to BofA data.

“The gap between price and intrinsic value is high, based on snapshot P/E multiples,” Subramanian admitted. “But the ex–Magnificent Seven trades closer to long-term average multiples, and, more importantly, today’s index lacks comparability to prior decades’, in our view.”

The veteran strategist noted that highly valued Big Tech stocks are obscuring the true valuation of the overall market. To her point, the Magnificent Seven—a group that includes Microsoft, Google, Apple, Nvidia, Tesla, Meta, and Amazon—trade at roughly 38 times their trailing 12-month earnings, compared with 23 times for the S&P 500 as a whole.

Subramanian also pointed out that the S&P 500’s constituents are quite different from what they used to be, which makes comparing the index’s valuation with its historical average less valuable.

“Valuation matters. But comparing a trailing P/E today to a trailing P/E of prior decades makes little sense given the index’s mix shiſt,” she wrote. “Today’s S&P 500 is half as levered, is higher quality, and has similar or lower earnings volatility than in prior decades.”

But are investors too euphoric?

The second most common feature in any stock market bubble is euphoria. And surging AI stocks, led by the 278% rise in Nvidia over the past 12 months, have some arguing that investors are pretty enthusiastic, but Subramanian used some of BofA’s data to push back on that idea.

She noted that U.S. equity investors’ excitement has been “ring-fenced” to themes like AI, but overall sentiment is “nowhere near bullish levels of prior market peaks.” In fact, investor sentiment is right around where it was in 1995, according to BofA data. “Sentiment is neutral despite pushback we hear that sentiment is ‘full bull,’” Subramanian wrote.

Overall, for Subramanian, despite the stock market’s surge over the past year, the S&P 500 “lacks signs” of a bubble. “In our view, this bull market has legs,” she wrote, adding “today is 1995, not 1999.”

The bears’ take

While Subramanian has made the case for the stock market to experience another banner year in 2024, there are always bears dishing out warnings. Just this week, Michael Gayed, a portfolio manager at Tidal Financial Group, told The Motley Fool that “we’re in a lot of trouble” and that “all bubbles end.”

Investment banks aren’t as worried about a true bubble, but there are a few big-name bears out there, including Morgan Stanley’s chief investment officer and chief U.S. equity strategist, Mike Wilson, who sees the S&P 500 dropping roughly 12% to 4,500 over the next 12 months. Wilson isn’t arguing we’re in a bubble, but he notes that 90% of the S&P 500’s “historic” 25% rally since October has been driven by rising valuations instead of improving earnings.

The CIO explained in a Monday note that he believes the market is being driven by “ambiguity” and “liquidity” this year, which means investors should remain vigilant for a correction.

As for the ambiguity part of the market equation, Wilson pointed to “conflicting data” in the economy and stock market that could be cause for concern. Strong economic growth with muted earnings; rising stock market valuations with a more hawkish Fed; these aren’t the typical combinations that you’d expect. Economic growth usually drives corporate earnings, and the threat of higher rates is supposed to decrease stock market valuations. So what’s to blame for the conflicting data?

“We think the current policy mix explains many of the disconnects that have been hard to reconcile from an economic, earnings, and performance standpoint,” Wilson wrote.

Federal government spending via the Inflation Reduction Act and CHIPS Act is driving spending and hiring by private construction and manufacturing companies, keeping economic growth alive, according to the Morgan Stanley CIO. But there’s an issue with this spending that could explain why earnings aren’t as strong as recent economic data: “While these programs are helping to keep the economy humming, they are also crowding out the private sector as they impact the cost of labor, materials, and capital,” Wilson said.

So Wilson’s “ambiguity”—or conflicting data points in the economy compared with the stock market—can partly be explained by rising federal government spending. But the second part of the equation is liquidity, which helps to explain the difference in the stock market’s strong performance compared with its relatively muted earnings growth, according to Wilson.

This is where the reverse repo facility comes in. In order to help pay for the federal government’s large budget deficit, the Federal Reserve allows private sector companies to earn a little extra money, often through an intermediary, by essentially lending money to the Federal Reserve overnight. These companies buy U.S. Treasuries and then agree to sell them back at a higher price at a later date, earning yield but providing the Fed with cash over a short term. This is used as a tool by the Fed to put a floor under short-term interest rates, but it also leads to rising liquidity. “In our view, that liquidity has helped to elevate asset prices broadly, led by some of the more speculative areas of the equity market/asset classes,” Wilson explained.

Wilson’s ambiguity and liquidity argument is a long, detailed way of saying “be careful” to investors, because the factors driving market gains may not be sustainable. “With these dynamics now better understood by the market, the burden is now likely on earnings/fundamentals to show more material improvement,” Wilson concluded.

This story originally Appeared on Fortune